A plain-language look at taxes

McCOOK, Neb. - For many residents, particularly young families and first-time homeowners, taxes are a reality paid regularly but rarely examined closely amid the demands of everyday life. Pay stubs, receipts and property tax statements arrive, some with little explanation of how the pieces fit together or where the money ultimately goes.

At the same time, McCook is undergoing a rapid series of development projects, many of which depend on residents contributing in one way or another.

In an effort to clarify confusion about tax sources and how public projects are funded, the Gazette has taken time during this quiet newsweek to break down the taxes most McCook residents regularly pay, how those taxes are structured and how the resulting revenue is used. A clearer understanding of those systems helps residents make sense of their finances and strengthens their ability, as voters and citizens, to evaluate local spending and public priorities.

Income Taxes

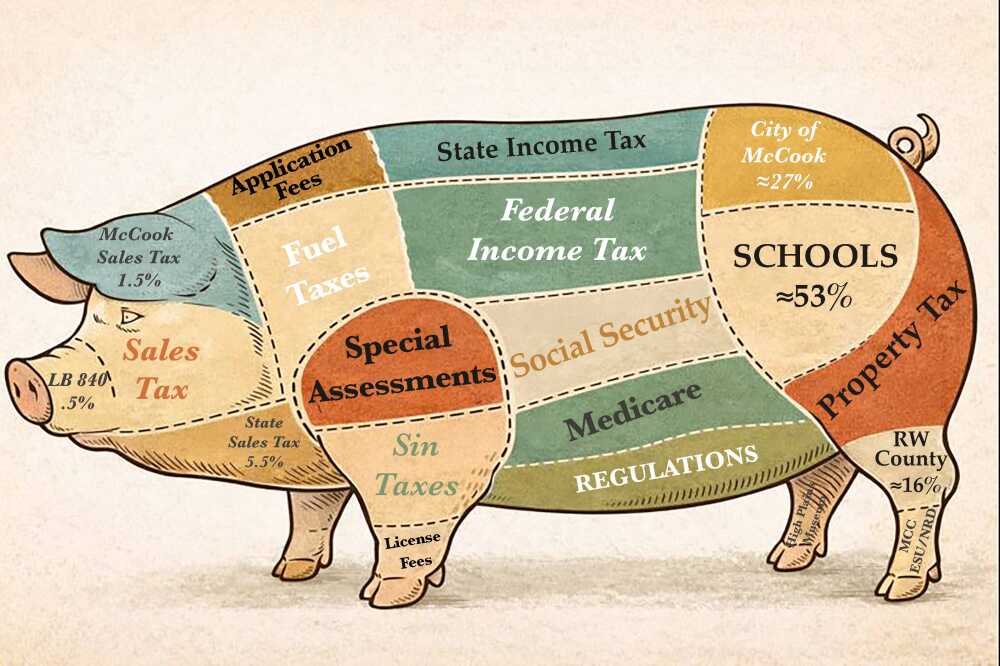

Federal and state income taxes account for the largest share of what most households pay. Federal income tax rates for 2025 range from 10% at the lowest levels to 37% for high earners, but because most incomes in McCook cluster near the local median of about $51,800, the vast majority of households fall into the 12% and 22% tax brackets. After standard deductions and the way brackets are applied, most local families end up with an effective federal income tax burden of roughly 10-15% of their income.

Nebraska�s state income tax is also structured in graduated brackets, ranging from about 2.46% to roughly 5.2% of taxable income. Revenue from the state income tax flows into Nebraska�s general budget, supporting statewide priorities such as education, highways and infrastructure, health and human services, law enforcement, and the court system. Because only portions of income are taxed at each rate, and because deductions apply, households near McCook�s median income typically fall in the middle of that range and end up with effective state income tax rates in the low single digits.

Property taxes

Property taxes are the most significant local tax for many households and businesses. Property taxes are among the oldest forms of taxation, with roots stretching back to medieval England and earlier systems that treated land ownership as a measure of wealth and civic obligation. Unlike income or sales taxes, which are tied to what people earn or spend in a given year, property taxes are based on ownership and reflect the principle that those who hold property have a stake in supporting the public institutions that protect and enhance it.

In Nebraska, property taxes apply across several categories of ownership, with real estate accounting for the largest share, followed by taxes and fees on motor vehicles and certain forms of business personal property. What distinguishes property taxes at the local level is that, rather than flowing upward to state or federal budgets, the revenue is divided among multiple local taxing entities.

On a typical McCook property tax bill, the largest share of the tax dollar goes to local schools.

In the example reviewed for this article, about 53 cents of every pre-credit dollar supports McCook Public Schools, reflecting Nebraska�s heavy reliance on property taxes to fund education. The City of McCook receives about 27 cents, funding police, fire, streets, and other city services, while Red Willow County receives about 16 cents for county operations, including the sheriff�s office, courthouse, and roads. The remaining few cents are divided among other local taxing entities, including the Natural Resources District, Mid-Plains Community College, Educational Service Unit 15, and a small levy supporting the Museum of the High Plains.

Motor vehicle taxes operate under a different system. In Nebraska, motor vehicle taxes are calculated under a uniform statewide framework, meaning the rules are the same regardless of where a vehicle is registered. Instead of using local property tax levies, the state bases the tax on a vehicle�s original manufacturer�s suggested retail price and applies a depreciation schedule that lowers taxable value as the vehicle ages. The tax is paid annually at the time of registration and, although collected by county treasurers, is set entirely by state law and does not vary between communities.

Personal property taxes, by contrast, remain part of Nebraska�s local property tax system, though their scope has narrowed significantly over time. Most household goods are exempt, meaning the tax primarily applies to business equipment, machinery and select commercial assets. Owners report the property�s value each year, and once assessed, it is taxed at the same local levy rates as real estate.

Sales tax

Nebraska collects a statewide sales tax of 5.5%, which is applied at the point of sale. While the tax is paid locally, it is managed at the state level, with most revenue flowing into the state general fund to support statewide services and operations. A smaller portion is dedicated to highways and infrastructure, and some state revenue is later shared with local governments through budget aid.

In addition to state taxes, McCook imposes local sales taxes that appear on receipts and remain in the community rather than flowing to the state. McCook�s general city sales tax currently stands at 2.0%, bringing the combined state and local rate to 7.5% on most taxable purchases.

Of that 2%, some of that revenue is dedicated to specific purposes approved by voters. In 2022, voters approved a separate 0.5 % sales tax increase to fund recreational facilities, including a community swimming pool and sports complex. That tax is restricted to those specific projects�a water park and sports complex�and is set to sunset based on bond repayment or project completion.

City Manager Nate Schneider explains that the remaining 1.5% goes to �Keeping the property tax request as low as possible (sales tax dollars are put toward the general fund), paying down debt, capital projects and capital outlay.�

�Capital projects,� in this sense, would be street repair, drainage projects, park improvements, etc. �Capital outlay� would describe equipment or assets that are not buildings, but still have a long, useful life, like heavy equipment for streetwork, public safety vehicles, major facility equipment and technology.

Yet another voter-approved carve-out is incorporated into the 1.5% tax rate. Under Nebraska�s LB 840 Municipal Economic Development Act, 1/6th of McCook�s local sales tax (.033%) supports economic development programs administered locally and restricted to the uses described on the ballot.

In practical terms, the first 5.5 percentage points of tax on a purchase go to the state, the next 1.5 percentage points support general city operations and economic development, and the final half-point is reserved for voter-approved recreation projects.

Everything else

Beyond income, property, and sales taxes, most working households also pay federal payroll taxes for Social Security and Medicare. For employees, Social Security is taxed at 6.2% of wages up to a federal cap, while Medicare is taxed at 1.45% of all wages with no cap. Together, this means payroll taxes range from 1.45% at the low end to 7.65 % of wages for most workers. Because typical McCook household incomes fall well below the Social Security wage cap, the full 7.65% employee rate applies to the vast majority of local workers. The taxes are deducted automatically from paychecks, do not vary by location or filing status, and both the 6.2% Social Security and 1.45 % Medicare taxes are matched dollar-for-dollar by employers.

The stuff we don�t notice

Households also pay a variety of indirect and everyday taxes, collected incrementally and often unnoticed. Fuel taxes are embedded in the price paid at the pump and fund transportation infrastructure, including streets and highways. Utility bills commonly include occupation taxes or franchise fees passed through by electric, gas, phone, cable or internet providers, ultimately supporting local government operations. Taxes on tobacco and alcohol are built into retail prices and help fund public health and general government programs. In some communities, residents may also pay local vehicle fees or wheel taxes tied to registration. Individually modest, these charges collectively represent a meaningful share of what households contribute toward public services each year.

Some residents will also encounter special assessments and improvement districts, which are not taxes in the traditional sense but are paid in a similar way. These include sidewalk, paving, sewer, and other infrastructure districts that fund specific improvements in defined areas. Unlike general taxes, these costs are charged only to the property owners who benefit directly from the project and are typically spread over time, making them targeted and temporary rather than part of the ongoing tax structure.

Just the beginning�

Beyond the above lie a broad category of taxes and fees that most households do not experience and therefore fall outside the scope of this overview. These include business-specific taxes, corporate income taxes, tariffs and trade policy, and regulatory fees tied to licensing, permits, and compliance. While these charges play a role in government finance and economic policy, they are generally paid by businesses or specific industries and warrant separate treatment.

Taken together, these taxes fund the basic services people rely on every day � from roads and schools to clean water, public safety, courts, and public health � even when those systems are largely taken for granted. As voters, citizens, and taxpayers, understanding how these taxes work and where they come from provides insight into personal finances and helps inform decisions at the ballot box.